TIL adalah singkatan dari Today I Learned. Rubrik impulsif yang gue buat untuk tulisan mingguan edisi hari ini. Di sini gue menulis penjelasan singkat istilah baru seputar startup, teknologi dan fintech. Nama TIL terinspirasi dari subforum reddit yang sering gue baca.

Di TIL edisi hari ini, gue akan menjelaskan istilah pasar modal yang sedang hits di Silicon Valley : SPAC.

SPAC adalah singkatan dari Special Purpose Acquisition Vehicle. Definisinya adalah perusahaan publik khusus dibuat untuk keperluan akusisi. SPAC mengalami proses IPO seperti biasa, tercatat di pasar modal tetapi dia tidak mempunyai kegiatan operasional bisnis dan didesain untuk menjadi “wadah kosong” yang akan di “tempati” perusahaan yang akan di akusisi.

Setelah merger terjadi, SPAC melebur menjadi perusahaan yang diakuisi dan tetap tercatat sebagai entitas di pasar modal tersebut.

Akhir-akhir ini, Beberapa perusahaan terkemuka go public menggunakan SPAC. Salah duanya adalah maskapai Virgin Galactic dan startup truk elektrik Nikola. Tren menjadi semakin hangat setelah beberapa investor besar mendirikan SPAC mereka sendiri sebagai wadah investasi kedepan. Nama-nama besar seperti pendiri Linkedin Reid Hoffman, mantan eksekutif awal Facebook Chamath Palihapitiya dan investor bilyuner Wall Street Bill Ackman.

SPAC dianggap alternatif yang lebih cepat dan lebih murah dibandingkan IPO konvensional.

Akan tetapi SPAC juga lebih beresiko, karena investor mempercayakan uangnya sebelum proses akuisisi terjadi. Seperti urunan naruh duit di topi pas lagi nongkrong. Lo gak tau uangnya bakal dipake apa. You just have to believe sama temen lo yang ngumpulin duit.

Gue belum tahu aturan detail mengenai SPAC atau yang setara di pasar modal Indonesia. Tapi melihat tren di US, sepertinya model go public alternatif seperti ini menjadi opsi menarik untuk startup-startup unicorn lokal. Unicorn seperti Gojek, Traveloka dan Tokopedia belum ada yang go public.

Startup teknologi yang baru masuk bursa akhir-akhir ini adalah Cashlez.

Apakah Wilson Cuaca akan membuat SPAC di Indonesia ? Lets wait and see.

Referensi lebih lanjut mengenai SPAC, bisa dibaca di link berikut :

Demikian untuk edisi perdana dari TIL. Klo lo ada ide istilah asing apalagi yang bisa gue bahas di edisi berikutnya, komen aja disini atau mention @kikiahmadi di twitter. Thanks!

Terima kasih telah membaca artikel ini. Jika kamu menikmati tulisan ini dan ingin mendapatkan update tulisan terbaru, artikel / podcast / video youtube dan juga musik menarik yang aku rekomendasikan, sila subscribe email list dibawah.

Processing…

Success! You're on the list.

Whoops! There was an error and we couldn't process your subscription. Please reload the page and try again.

Seri pivot pandemi ini merupakan tulisan bagaimana bisnis bertahan menghadapi COVID-19. Post ini adalah hasil brainstorming dengan beberapa teman dari berbagai macam industri. Semua seri Pivot Pandemi bisa dibaca di link berikut.

Setelah sebelumnya membahas bisnis tradisional, Pivot Pandemi kembali membahas tech startup. Di edisi ketiga, gue ngobrol bareng teman lama dari kuliah, VP startup SaaS untuk manajemen supply chain. For the rest of the article, kita sebut startup ini sebagai Startup 123. Lets go!

Ive been managing a business development (BD) team for 3 years now. During this time, i see that BD role can meant different things. In some companies, the role skews more to sales, in other it might be more to product development. There also stark difference from BD in big corporate versus in startup. The first one might be more to high-level strategic partnership, while the latter more hands-on with business operations and expansions.

In Amartha, i can summarize my work as developing new business by pushing ideas into rollout. In this post, ill share several of my learnings developing new product / business, starting from brainstorming scribbles in notepad, work the ideas into concept slides, running a pilot and finally decide to expand it in multiple areas.

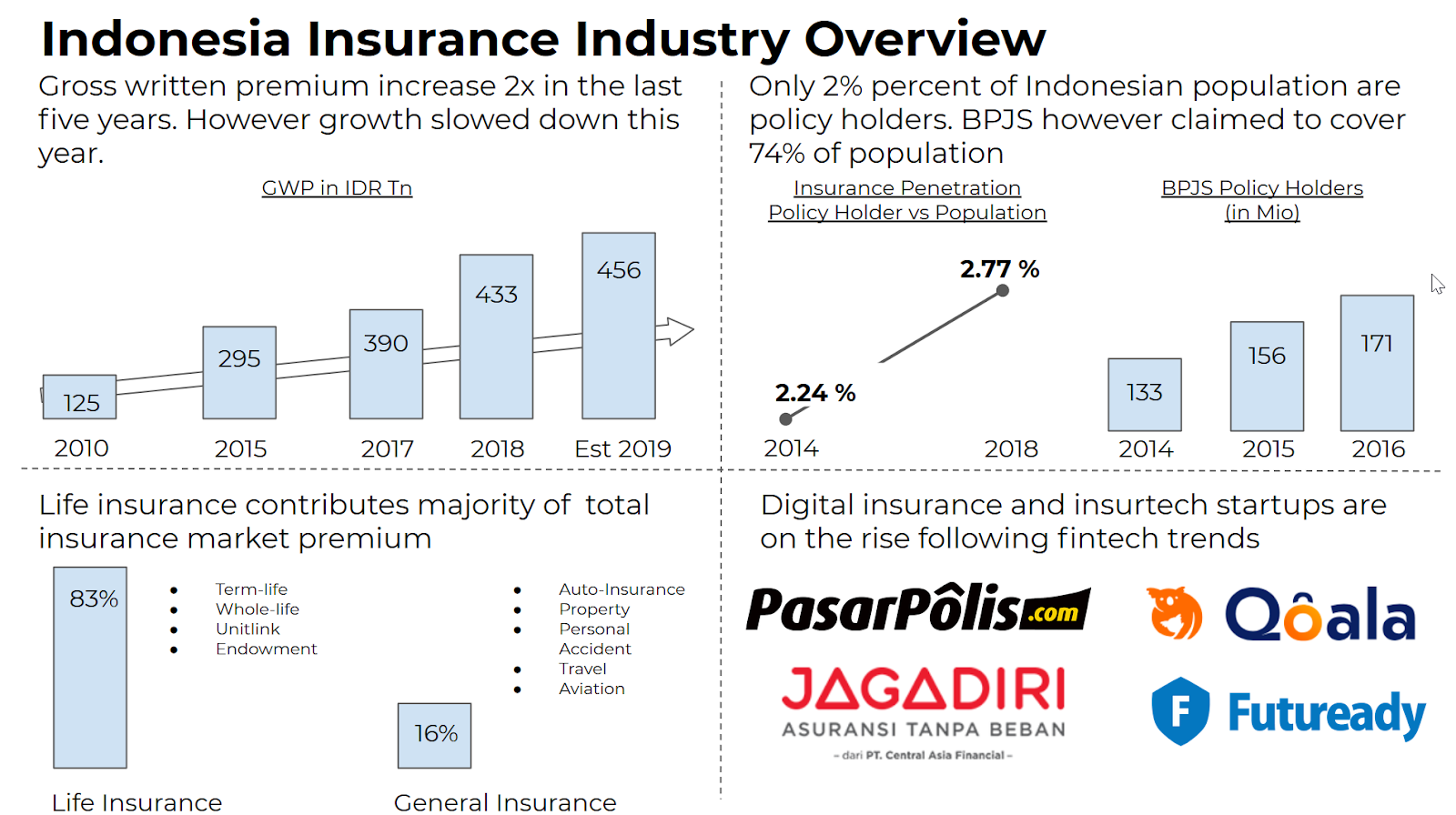

In the past decade, the insurance industry in Indonesia has been growing from IDR 125 trillion in 2010 up to nearly IDR 500 trillion this year. Despite this growth, penetration in population is still very small. In terms of economic contribution,, insurance spending only account for 2.3% of GDP while the number of private insurance policy holders also less than 3% of the population. In 2014, national health insurance (BPJS Kesehatan) was established by SBY Administration. Current coverage for this is estimated around 75% of population or ~180 million people. With the rate of growth and low penetration of private policy holders, Insurance market in Indonesia is a massive untapped opportunities.

Current market value are still majority contributed from Life Insurance. Based on Insurance Association data, more than 80% of gross written premium are from Life Insurance product such as Term-life, Whole-life and Investment Bundled Product (Unitlink). Unit Link is the most sold product of all life insurance, with contribution of more than half of premium sold in 2014. For general insurance, market size are driven by car and motorcycle insurance.

In terms of distribution and sales channel, majority of insurance sales are still driven by agents and banc assurance. Agent solve the needs of consultation and product knowledge due to the complexity of insurance products. While for banc assurance, insurance companies are helped by bank agents and customer services to advocate their product to banks existing customer base.

Recent surge in insurtech makes many people buy insurance online. However they mostly buy simple, one-time product such as flight, delivery or gadget insurance which have simple straightforward policy. Price is usually very cheap as well. Online channel drive high-frequency, low-value transactions. Hence in terms of total market gross premium value, it will still likely contributed by life-insurance sold by agents.

Insurance principal can be divided into two big categories : Life insurance and general insurance. Both have distinct market dynamics. Life insurance are quite concentrated with Prudential as clear market leader. Most of the big players in Life Insurance also foreign entities such as Allianz and Manulife. General insurance on the other hand is quite fragmented with Sinarmas, Jasindo and Astra closely competing to be top 3. Sinarmas and Astra premiums are driven by auto and property insurance while Jasindo and other state-owned insurance (Tugu, Askrindo) are contributed by industry insurance supporting other SOE (e.g Marine, Oil & Gas insurance).

Key Insurance Players Overview in Indonesia

With low market penetration and sales mainly driven by offline channel, Insurance market are just prone to be disrupted by digital players. From big insurance principal who goes digital up to rising startup who try to break through using innovative products.

In the past years, there is a rising trends of startups and companies which aim to digitize traditional retail merchants a.k.a Warung.Kudo pioneered this back in 2014. They then acquired by Grab in 2017, and recently rebranded into GrabKios. Next is E-commerce unicorn Bukalapak who dove in in this space big time by launching Mitra Bukalapak in 2017. Mitra Bukalapak is estimated to have 3 millions registered user which makes them market leader in digital warung. Tokopedia followed on by launching Mitra Tokopedia in 2018. There are also smaller players such as East Venture backed, Warung Pintar, KiosOn and Payfazz.

This warung trend apparently not only happening in Indonesia. Amazon last week just announced their move to partner with thousands of kirana store, Indian version of warung, to be used as delivery hub. Jeff Bezos himself came down to India to launch this. There is also Mastercard which enabling multiple initiatives to digitize mom-pop store in Latin America.

In this article, i dive into the reason why the trend is happening and which direction will warung digital going to go in the near future. Lets go!.

Quick recap on attending what probably the biggest tech and startup conference in South East Asia. I only attend day 2 hence this might be short. Hopefully still useful.

Enjoy!

View from the front seat

Xendit on Running Experimentation and Hiring Practices

Moses Lo and Tessa Wijaya from Xendit shares their experience scaling startup beyond series A. Xendit itself is a payment gateway, enabling apps or website to do everything related to payments.

First interesting insight from them is their dead simple guidelines on running experimentation : 3 months, 7% growth per week. Any experimental product which consistently passing those bar will get invested more. Below the bar, project will be scraped. Nothing happened to the team, they will be assigned for something else. Any point of time, Xendit will have 3 or 4 “business as usual + 1” experiments , new product which adjacent to their current offering.

This is a good innovation practice by nurturing exploration while still budget conscious. Moses learned this from his time in Y Combinator.

Second one is their hiring practice to do trial day. Candidates applying for Xendit will have to spend one day to work with the team as part of their hiring assessment. By doing this both the team and candidates can sense whether they can fit together or not. Since interview is a bad predictor of performance, Trial Day help Xendit avoids bad hiring by test the candidates on real working condition.

OVO on Solving Problems Using Fintech

On main stage, Jason Thompson from OVO delivered quo vadis speech on where the fintech is going. It was the best presentation ive seen on Day 2. Jason gave insightful and humble presentation on OVO’s journey so far.

Three key points from Jason’s speech.

First, OVO achieved 10x growth due to strategic partnership with Grab and Tokopedia. Grab Bike & Grab Car contribute high frequency of transactions while Tokopedia drives the value of the transactions. On top of that, OVO itself boost ubiquity and reason to use by having presence in almost every shopping mall in Indonesia.

Jason Thompson, CEO of OVO

Second, answering on the skepticism on cash-back, the growth of OVO has been healthy. This is due to the growth in both users and value, is followed by growth in stored value fund. Seems like users are more comfortable to left their money in OVO balance.

Third, OVO aimed to expand beyond wallet into other financial services. Investment will be their first expansion, powered by Bareksa acquisition. Jason spent quite a time emphasizing how big investment opportunities in Indonesia while investment in adoption is still very low compared to the region.

Massive opportunities in Indonesia investment market

Lending and insurance will be next. OVO transaction data will be leveraged to make their financial services attractive for each users ( e.g credit scoring for cheaper lending and insurance).

And yes, Jason also confirm OVO status as the fifth unicorn in the country.

Tokopedia on Their Next 10 Years

William Tanuwijaya interview was probably the most sought-out session in Day 2 of the conference. Main stage area was jam-packed with people, i could barely saw the stage.

William, Tokped founder versus Willis, TIA founder

Guided by Willis Wee of Techinasia himself, William talk about a decade of Tokopedia journey, key decisions thats important for growth of Tokped and also his personal growth as a founder CEO.

Three important takeaways for me.

First, asked about early decisions that has been pivotal for Tokped foundation, Willliam answer was the decision to not blindly copy global ecommerce promotion day (e.g 11.11 in China, Black Friday). Relying on big-bang promotion day to boost sales is not only unsustainable, but also many of these promotion day is out of context for Indonesian hence it doesnt bring good result. Tokopedia choose to pick promotion day on the last week before lebaran. Smart move considering most office workers already got their THR bonuses during this time. This is also a subtle jab for Bukalapak which make promotion day every single month (1.1, 2.2 and so on).

Second is about their Super Ecosystem strategy. Tokped is exploring many new things such as financial services, selling tickets and bill payment. However, William emphasized that Tokopedia will prefer collaborate with aligned partners rather than building their own. Different path from what Amazon is going where they start to develop many in-house verticals. Hence Tokped platform will be geared to be more open and William invites startups and other institutions to develop the ecosystem together.

Last and the most interesting one is his vision on Tokped next 10 years. Tokopedia next decade vision is to enable smalll business owners in rural Indonesia to have the same capabilities as national (or international) retailer. William cited that he wants store owner in Aceh can possibly make their business big without having to move to Jakarta to get better access to market. This could contribute into decentralization of economy of Indonesia and also reverse urbanization.

To realize this vision, Tokopedia will make most of their e-commerce capabilities as a services for this small business. For example, if a seller need logistic or warehousing capabilities to do overnight delivery, Tokopedia could provide it. This also goes for marketing, payment and other capabilities.

In their last impact report, Tokopedia claimed to contribute 1% of Indonesian economy. William aim to push this into 5% in the next decade.

This is series of study case analysis that i like to write from time to time. Check out my first post on Traveloka.

This week in fintech, state-owned e-wallet provider T-CASH announced that they will transform into LinkAja. Not only the name change, the new T-Cash will be backed not only by Telkom group but also six other state-owned enterprise (SOEs) : Bank Mandiri, BRI, BNI, BTN, Jiwasraya and Pertamina. The change will be implemented late February and current T-Cash users will only need to update their app once LinkAja launched.

T-cash QR Payment feature. image credit from kanalaceh.com

Ini adalah thread quorayang saya jawab beberapa waktu lalu. Platform Quora ini cukup menyenangkan dan saya aktif disana. Cek kesini untuk melihat semua jawaban yang saya tulis.

Skena dari film The Founder dimana Michael Keaton memerankan Ray Kroc

Di satu konferensi, saya berkesempatan mengobrol dengan Pak Jefrey Joe dari Alpha JWC Venture. Seorang venture kapitalis yang portfolionya bisa dilihat dilink dibawah

Ini sebenarnya adalah thread Quora yang saya jawab beberapa waktu lalu Karena responsnya cukup bagus, saya menambahkan beberapa materi dan memposting ulang disini.

Platform Quora ini cukup menyenangkan dan saya aktif disana. Cek kesini untuk melihat semua jawaban yang saya tulis.

I cant believe how fast 2018 have been going for me. I went lot of new challenges, good thing most of them turn out quite well. In 2018, I’ve ventured into new areas at work, managed bigger team and took terrifying steps into the big financial commitment (i bought a house on mortgage). Been hell-a-lot of personal developments which was exciting and scary at the same time.

Three good books i recommend to read

Speaking of personal developments, ill share top three great books that I’ve read last year with interesting points from each. These books helped me find perspective and calmed me down during roller coaster ride. I hope this list give you ideas on what to read to start your 2019 right.