To accompany this blog posts, i created also report version of this in presentation form.

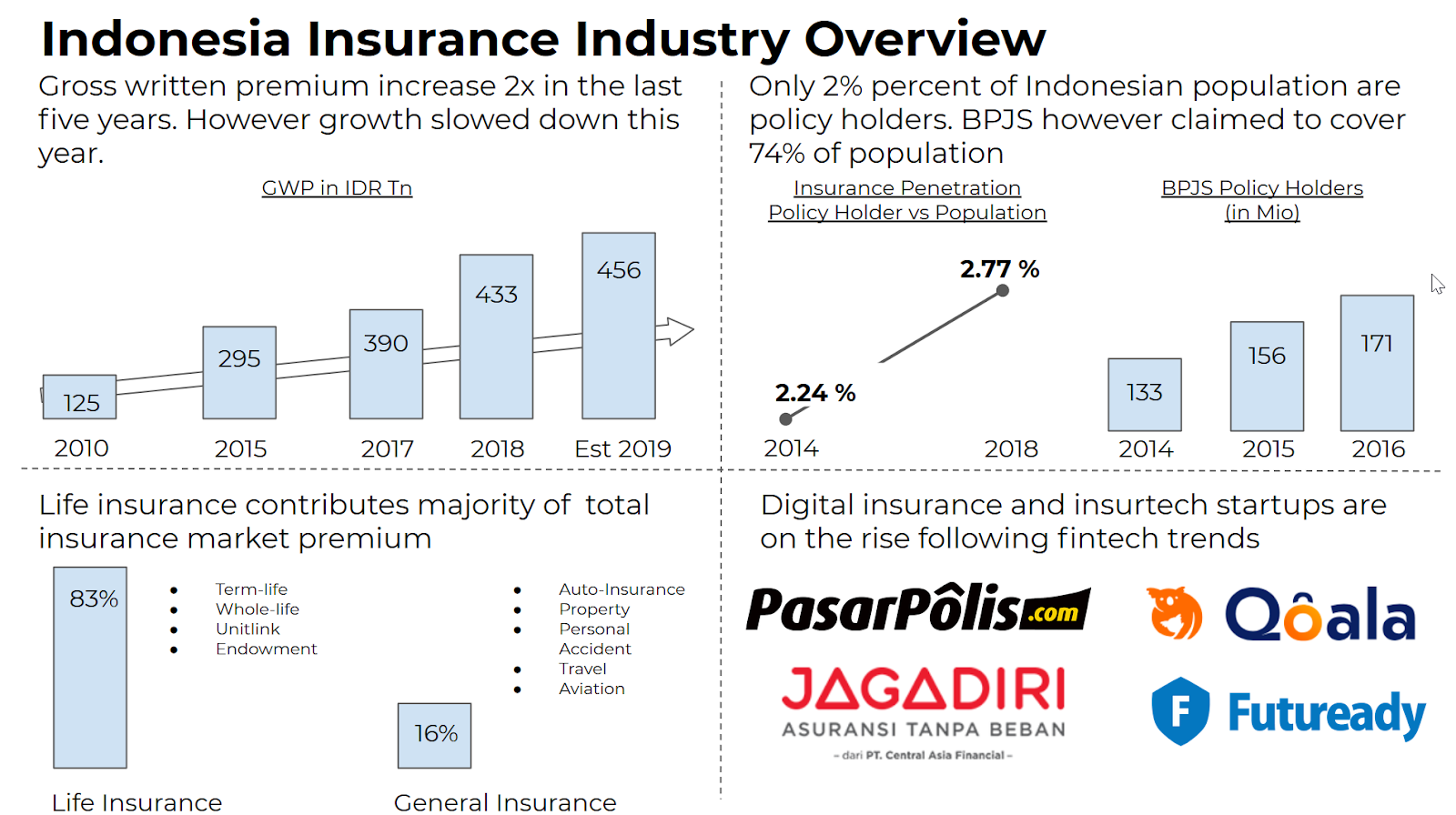

In the past decade, the insurance industry in Indonesia has been growing from IDR 125 trillion in 2010 up to nearly IDR 500 trillion this year. Despite this growth, penetration in population is still very small. In terms of economic contribution,, insurance spending only account for 2.3% of GDP while the number of private insurance policy holders also less than 3% of the population. In 2014, national health insurance (BPJS Kesehatan) was established by SBY Administration. Current coverage for this is estimated around 75% of population or ~180 million people. With the rate of growth and low penetration of private policy holders, Insurance market in Indonesia is a massive untapped opportunities.

Current market value are still majority contributed from Life Insurance. Based on Insurance Association data, more than 80% of gross written premium are from Life Insurance product such as Term-life, Whole-life and Investment Bundled Product (Unitlink). Unit Link is the most sold product of all life insurance, with contribution of more than half of premium sold in 2014. For general insurance, market size are driven by car and motorcycle insurance.

In terms of distribution and sales channel, majority of insurance sales are still driven by agents and banc assurance. Agent solve the needs of consultation and product knowledge due to the complexity of insurance products. While for banc assurance, insurance companies are helped by bank agents and customer services to advocate their product to banks existing customer base.

Recent surge in insurtech makes many people buy insurance online. However they mostly buy simple, one-time product such as flight, delivery or gadget insurance which have simple straightforward policy. Price is usually very cheap as well. Online channel drive high-frequency, low-value transactions. Hence in terms of total market gross premium value, it will still likely contributed by life-insurance sold by agents.

Insurance principal can be divided into two big categories : Life insurance and general insurance. Both have distinct market dynamics. Life insurance are quite concentrated with Prudential as clear market leader. Most of the big players in Life Insurance also foreign entities such as Allianz and Manulife. General insurance on the other hand is quite fragmented with Sinarmas, Jasindo and Astra closely competing to be top 3. Sinarmas and Astra premiums are driven by auto and property insurance while Jasindo and other state-owned insurance (Tugu, Askrindo) are contributed by industry insurance supporting other SOE (e.g Marine, Oil & Gas insurance).

With low market penetration and sales mainly driven by offline channel, Insurance market are just prone to be disrupted by digital players. From big insurance principal who goes digital up to rising startup who try to break through using innovative products.

Rise of Insurtech

There are three main types of insurtech : Digital Insurance Principal, Insurance Broker and Comparison Services.

Digital Insurance Principal usually are either spinoff or digital channel of a conventional insurance companies. Realizing the fintech wave, these incumbents develop new insurance entities which can have full online process from consultation, purchase and claim. Prominent examples are Simas Insurtech from Sinarmas, Ilovelife from Astralife and Jagadiri from Asuransi Central Asia (ACA).

Insurtech startups mostly are digital insurance broker. They curate multiple insurance products from principal and sell it through their digital channel. Insurance product sold by these players are mostly micro-insurance with straightforward policy. Most digital insurance brokers also integrated with e-commerce or e-wallet platforms. Leveraging third-party platform, insurtech brokers provide seamless insurance purchase experience. Players within this category are : Pasarpolis, Qoala, Futuready and Fuse.

Last but not least are Insurance Comparison Services startups. Different from brokers, these startups only provide comparison and redirect it to respective principal website. Usually comparison services like this not only focus insurance but also other financial services such as Lending, Mortgage and Credit-cards.

Highlights on Key Insurtech Players

PasarPolis

PasarPolis or Paspol is a Jakarta-based insurtech startup founded in 2015 by Cleosent Randing who previously founded performance marketing firm Valuklik. It was originally was a comparison site, but they pivoted into micro-insurance. Paspol became prominent after offering auto-insurance to Gojek and Gocar drivers. Paspol then solidify its position when they was invested by three unicorns : Gojek, Traveloka and Tokopedia in August, 2019. Amount of funding was undisclosed.

PasarPolis offer Travel, Gadget and Auto-Insurance. Most of PasPol services are integrated into Gojek, Traveloka and Tokopedia. PasPol is also operated in Vietnam and Thailand (Gojek operations), with development office in India.

They claim to process up to 2 million policies per day. With this number, Paspol might be the market leader in Indonesia insurtech.

Qoala

Qoala is an insurance aggregator startup founded in 2018. They started specifically in travel and flight insurance but has been expanding to gadget, health and P2P lending insurance. It recently raised 1.5 million seed round, led by Sequoia India (Surge).

Qoala offer 3 value props : 1 day claim, no paperwork at all and seamless paying experience. Similar to Paspol, Qoala offers Flight, Gadget and Micro-Health insurance through integration with e-commerce such as Tokopedia and Bukalapak. Qoala user can also download the app and check all of their policies in one place even though they bought it in multiple platforms.

Simas Insurtech

Launched in 2015, SimasNet or Simas Insurtech is a digital insurance spin-off from Asuransi Sinarmas. In Insurtech industry, SimasNet probably the most integrated insurance principal. They are integrated to insurtech broker such as PasPol, Qoala and fuse, comparison services like Cermati and GoBear, and direct integration with platforms such as Traveloka.

In 2018, SimasNet achieved IDR 54 billion gross premiums. By June 2019, they have achieved that number with targeted FY 2019 gross premiums of 100 billions. An impressive double digit growth contributed solely from digital channel.

Points of Conclusion

- Insurance penetration in Indonesia is still less than 2% of population. Market share of premiums are primarily contributed by life insurance with sales driven by agents.

- Three main barriers of accessing insurance in Indonesia. Awareness : product is often complex to understand. Access : Consumer need to have access to agents or have bank accounts. Affordability : Premiums are expensive and need long payment commitment.

- Insurtech drive insurance sales through simple-micro insurance product and integration with E-commerce platforms. Market leader so far is PasarPolis due to their integration with Gojek, Tokopedia and Traveloka.

Thanks for reading. Complete references, links and further readings can be read in this presentation. Special thanks to Adjie Wicaksana for the ideas and discussion which inspired this blog post.

If youre enjoying this post and want to get updated content via email, subscribe via form below

Halo, assalamu’alaikum mas Kiki

Terimakasih buat posts nya dan juga untuk insurance industry, very insighful and amzing contribution.

Maaf saya ingin cek untuk data GWP yang ditunjukkan, sepertinya berbeda dengan data OJK, e.g. di 2019 total GWP Rp 249T. Apa boleh dishare sedikit sumbernya?

Thanks

Rahmat

Muaman Sharia Insurtech